Building the World's Best Venture Firm

Founders take note

When I joined Vine Ventures as the first hire a little under three years ago, I asked myself what it would take to build the world’s best venture fund. A lot was at stake – not just me and my colleagues’ careers, but the capital from our limited partners and the relationships with our future founders.

The last three years have been the best kind of whirlwind. We are now the second-largest seed-stage venture fund based in New York with additional offices in San Francisco and Tel Aviv, and we are proud long-term investors in over 25 exceptional companies led by high-integrity, problem-obsessed founders.

I wanted to share this info at the start of this blog post for two reasons. First, I’m excited to announce my recent promotion to partner at Vine. It’s an honor to have built such wonderful trust among my colleagues, founders, and broader community, and I couldn’t be more fired up for the journey ahead. And second, I wanted to revisit the same question I asked myself three years ago – what does it take to build the world’s best venture fund – and share a few thoughts.

The funny thing about this question is that very few investors ever seem to ask it. At any moment in time, there are a handful of key challenges that impact the venture ecosystem. Some of these challenges are exogenous – for example, the fact that valuations for exciting AI technologies are high or the fact that there are so many venture funds competing for too few compelling deals. In my experience, these exogenous variables are the only ones that people talk about, and they’re also the least addressable.

What I find more important – and yet rarely discussed – are the endogenous challenges in VC. These are the internal variables at a VC firm, the same variables that we, at Vine, have been tweaking and adjusting as we scale.

I strongly believe the following to be true: the vast majority of VC firms are severely self-unoptimized, meaning they construct and run themselves in a way that is detrimental to operations and returns. Unlike exogenous variables, endogenous variables are fully within VC firms’ control, which is why it is surprising that they have addressed them inadequately.

I realize this post will be more “VC-ey” than normal and that most of my subscribers are founders. This is by design. I believe it’s incredibly important for founders to be aware of these dynamics, as working with a “self-optimized” VC will produce a far better partnership than working with one that is “self-unoptimized.” I will circle back to this point at the end.

Endogenous Variables in VC

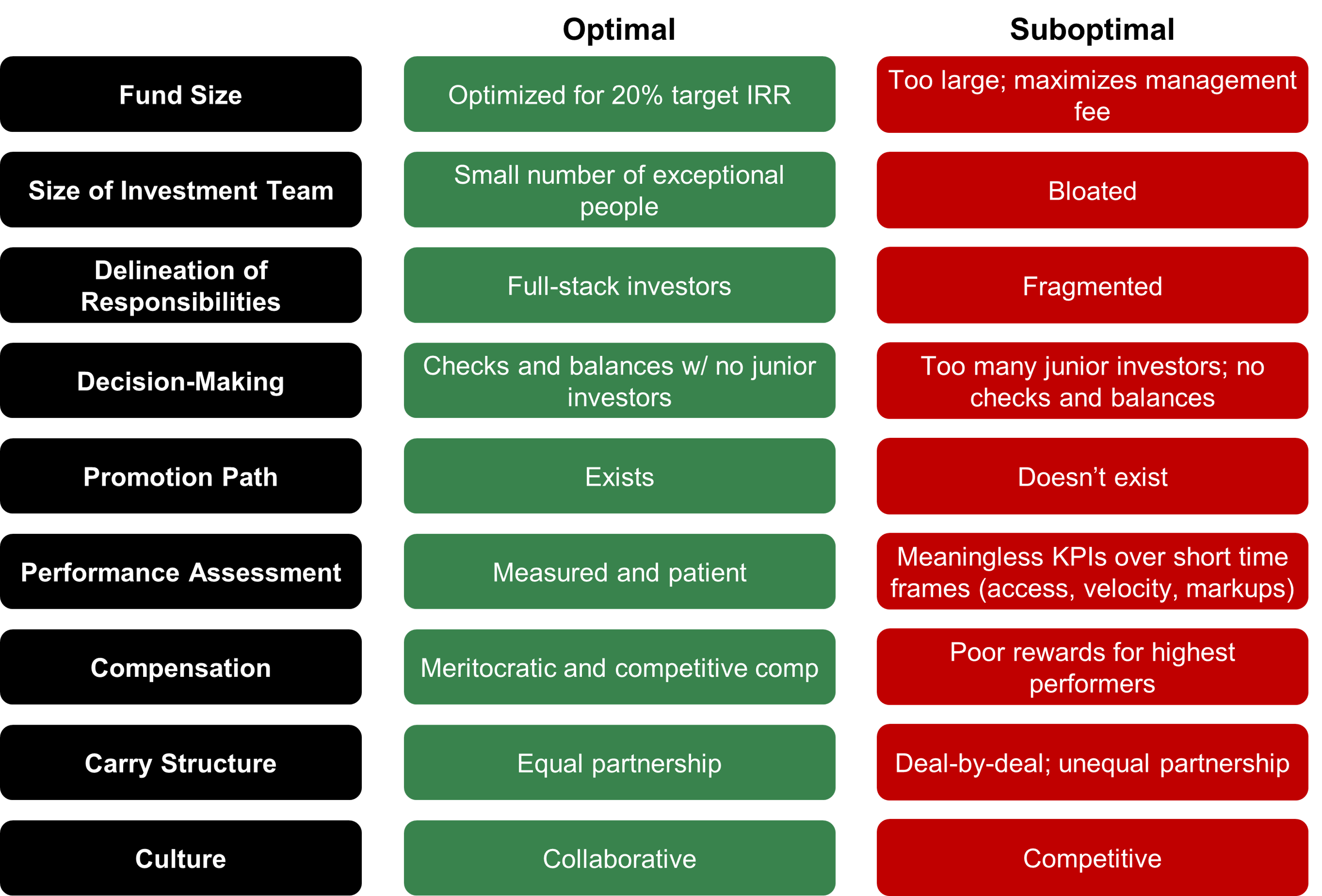

The following represents my list of key endogenous variables that matter to a VC, and that are often significantly self-unoptimized.

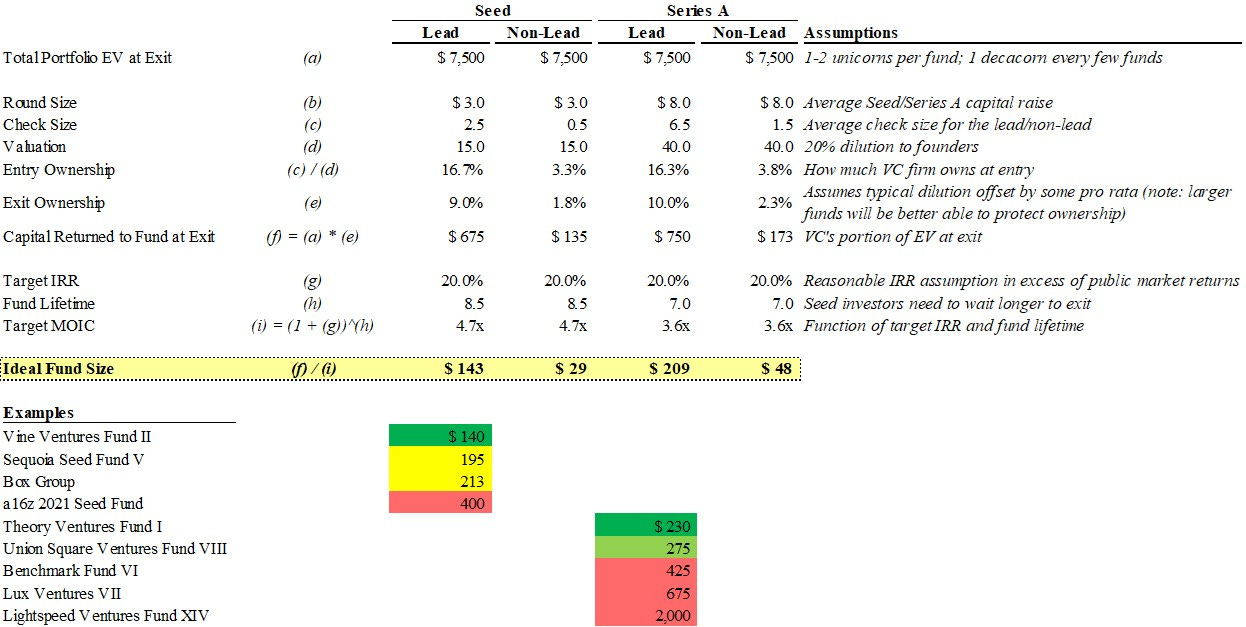

Fund size: In theory, it’s common knowledge that fund size equals fund strategy. In practice, many VCs treat these concepts as separate. There are many factors that drive VCs to increase fund size beyond reason, but a combination of overconfidence in ability and desire for more management fees are the usual culprits. But what constitutes the “correct” fund size for a given strategy? The key input is a reasonable assumption of the total enterprise value of a venture portfolio at exit. Let’s create an illustrative example for Seed and Series A funds. Let’s say $7.5bn is your assumption for average total EV at exit because you expect to hit ~1-2 unicorns per fund and a decacorn every few fund cycles. With this as a starting point and a few other simplifying assumptions we can estimate the following ideal fund size for Seed and Series A firms (separated by those who lead and don’t lead deals). For fun, I then show how a few well-known funds stack up to these figures. As you’ll see, some fund sizes make sense relative to the returns they promise, and others do not.

Size of investment team: VC firms should strive to hire the absolute minimum number of investors needed to identify and invest in the best technology companies for a given strategy. Bloated teams slow down decision-making processes, reduce overall talent quality, can frustrate high-performers and incentivize them to leave, and force people to spend time on nonessential workflows and opportunities. Bloated teams will also exacerbate many of the other factors that I’m about to discuss in more detail (e.g., delineation of responsibilities, decision-making, promotion path, compensation, etc.).

Delineation of responsibilities: How are responsibilities split within a VC firm? Are the employees who source deals different than those who invest in a company? Is the person who knows the founder’s business on the board, or was that responsibility given to a more senior partner? Do the investors have direct relationships with relevant operators, or is that handled by someone on the platform team? At Vine, we aspire to be full-stack investors, a term we use to describe someone who can source an investment, run point on diligence, sit on the board post-investment, and introduce founders to potential customers and hires, among other responsibilities. Too many firms fragment responsibilities among too many people. While it may be easier to build this kind of VC firm (e.g., it’s easier to hire someone who is good at one thing vs. good at many things), it inevitably results in founders receiving fragmented and inconsistent value from their investors.

Decision-making: Who makes investment decisions at a VC firm? From the founder’s perspective, it’s important that the person who best understands your business has the most influence on the final investment decision (otherwise you’re wasting your time). From the VC’s perspective, it’s important that processes are in place to ensure that decisions are more right than wrong. Too many VC firms have junior investors who are closest to an opportunity but furthest from the final investment decision. Furthermore, too many VC firms have broken decision-making processes, either by giving individual partners too much leeway to call their shots or overconcentrating decision-making power to the whim of a single GP. Instead, perfecting the decision-making process requires a system of checks and balances, where a deal partner has the most informed and respected voice in the room, but where the voices of other partners on a diverse investment committee can approve (or veto) the deal partner’s recommendation.

Promotion path: Many VC firms do not offer a clear path to promotion for junior investors. This is a huge mistake. If potential for promotion explicitly or implicitly does not exist, then junior investors may make decisions that are fundamentally antagonistic to fund goals. For example, it is common for junior investors to recommend highly competitive, overpriced investments and then use that track record to pivot to another fund before they can be evaluated on those deals.

Performance assessment: To run a successful company, it’s important to retain top-performers and let go of poor-performers. However, most VC firms struggle to assess performance. If you’re trading liquid assets and have a short investment duration (e.g., a long-short public equity hedge fund), it’s more intuitive to track an investor’s performance. But venture capital deals with illiquid assets over incredibly long durations – often success (or failure) is over a decade away. Consequently, most VCs assess performance on 1) deal access, 2) velocity of deals, and 3) markups. But these measures can be misleading. Good access often means you’re seeing the same deals as everyone else (i.e., no alpha), doing a lot of deals means nothing if those deals do not generate returns, and paper markups can diverge significantly from underlying business health. Generally speaking, it is the crossover funds and the funds with the most competitive internal cultures who struggle to correctly assess performance because they default to applying the same methodology of performance assessment across their public and private deal teams.

Compensation: Building a world-class venture firm requires world-class talent, but world-class talent is expensive and hard to retain. VC firms tend to make three common mistakes when it comes to compensation. First, GP’s often will allocate too much compensation to themselves relative to high-performing employees. Inevitably, the high-performing employees realize that they are better off joining another firm that is more meritocratic or spinning off to start their own fund. Second, GP’s will pay well on salary but not allocate enough carry to their high-performing employees. Not only is the upside potential associated with carry higher than cash compensation, but it locks in investors and makes them feel like true owners of their fund. Third, GP’s fail to recognize junior talent and over allocate compensation to underperforming senior talent. Funds that have been around for a long time most often run into this problem, and often struggle to share upside with junior employees who are responsible for the go-forward success of the firm.

Carry structure: Carry structure is related to compensation but deserves a separate section. Funds approach carry distributions to partners in different ways. In some cases, carry is allocated (or at least weighted) on a deal-by-deal basis – i.e., a partner is rewarded more for their deals and less for other partners’ deals. In other cases, carry is solely allocated to the GP, who elects to pay out large bonuses to partners at his/her discretion. Lastly, in rare cases, the fund is an equal partnership, meaning all carry is evenly split between all partners at a fund. This last approach, in my opinion, is optimal. It fully aligns partners’ incentives with the incentives of the fund and creates a collaborative environment between the decision-makers at a fund.

Culture: In an ideal world, VC firms have collaborative internal cultures, where partners are supportive of each other and each other’s portfolio companies. Too often, however, VC firms inadvertently create highly competitive cultures, and partners operate out of self-interest.

Why Founders Should Care

What happens when a VC fund is self-unoptimized? More importantly, who should care about it?

For certain stakeholders, the consequences are more obvious. For example, VC funds that are self-unoptimized will struggle to retain key talent and will produce poor returns - two outcomes that are clearly not ideal for the fund itself and its limited partners.

But what about founders? Should they care whether a VC fund is self-optimized or not? When I ask what kind of VC a founder is looking for – I rarely hear about any of the variables I’ve discussed in this post. Instead, I hear things like “I want a VC that can find me customers,” or “a VC that can help me hire,” or “a VC that understands my industry.”

To be clear, these asks are all super important. My point is not that founders should stop asking about customers, new hires, and industry-expertise. Rather, I believe founders should be asking more than that – specifically whether a VC firm knows how to run itself.

What are the consequences of taking money from a VC that is self-unoptimized? At a conceptual level, if a VC demonstrates it can’t run its own business well, I don’t believe they should be a in position to advise founders on how to run their own businesses. But I’ll also be more direct. Below are a few specific consequences founders face when partnering with self-unoptimized VCs.

Parting Thoughts

In this post, I’ve shown how VCs are self-unoptimized and how these dynamics impact founders. But I haven’t answered why funds self-unoptimize in the first place. Why should VCs choose to build their firms in ways that hurt returns? Moreover, why would LPs give self-unoptimized VCs capital?

In brief, there are multiple factors at play:

It takes a long time to validate or invalidate a VC’s strategy, largely due to the long fund cycles.

Many long-term suboptimal decisions are short-term enticing (e.g., receiving more management fees from a larger fund).

Maintaining an optimal state is difficult (e.g., maintaining a meritocracy, in terms of both compensation and decision-making, becomes increasingly more difficult as a firm matures, particularly given the natural generational turnover in technology).

Outside of fund size, LPs traditionally do not exert meaningful influence on the other variables. Maybe they should.

It’s just not on every GPs radar. I genuinely believe a lot of managers simply don’t think about these dynamics.

I titled this blog post “Building the World’s Best Venture Firm.” You’ll notice that I never mentioned that Vine is the world’s best venture firm. This is because I truly believe no one is a finished product. I do know, however, that we, at Vine, are obsessed with providing our founders the best user experience possible. And one of the subtle ways we do that is by constantly trying to self-optimize.